City Property Association’s 'City of London Market Update': Q&A with Dan Gaunt

Posted by Knight Frank Newcastle on 17th February 2025 -

Over two hundred developers, investors and real estate professionals gathered recently for an update on the current state of the London market, hosted by the City Property Association (CPA).

The event included a presentation from Dan Gaunt, Co-Head London Office Leasing at Knight Frank, and a panel discussion hosted by the chair of the CPA, Ross Sayers. We caught up with Dan to explore some of the key highlights from the morning…

Q: Dan, can you give us a brief overview of what you discussed during your presentation at the City Property Association event?

A: I spoke about the current state of the London market, covering both the investment and leasing sectors. I shared insights on how the investment market is performing, particularly around turnover and trends in buyer activity, and discussed the leasing market's strength, highlighting key demand drivers and recent trends in the City of London.

London Investment Market

Q: How is the investment market performing in London at the moment?

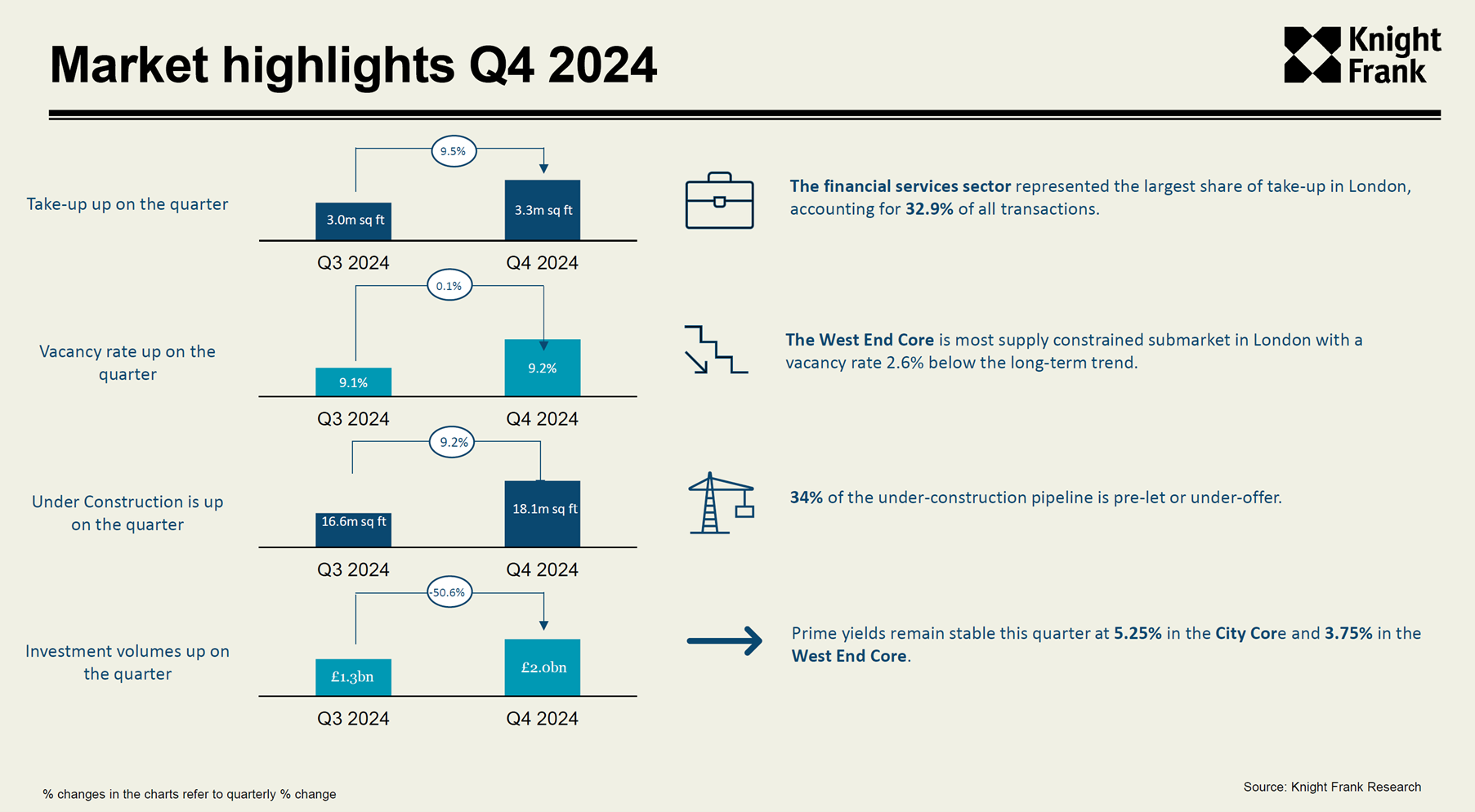

A: Investment turnover is currently 53.5% below the long-term annual trend of £13.2bn, which reflects a slower pace in comparison to previous years. However, Q4 saw an improvement, with investment volumes rising to £6.2bn.

Q: Who are the primary players in terms of investment nationality?

A: Investors from the United Kingdom continue to dominate, with £2.5bn in Q4. North American investors are the next biggest group, showing a continued interest in the London market.

Q: What types of investors are active in the market right now?

A: Private capital is still the most active. However, we've seen renewed interest from institutional investors, which signals growing confidence in the office sector, especially after a period where many institutional investors had withdrawn.

Q: What about prime yield stabilisation? What are the trends in that area?

A: In Q4, prime yields remained stable, continuing the trend we've seen for a while. Pricing for prime London offices has held up well, with prime net initial yields standing at 3.75% in the West End and 5.25% in the City and Southbank.

City of London Leasing Market

Q: How would you describe the current leasing market in the City of London?

A: The City leasing market is in a very positive state, and there’s still plenty of room for growth. The market has performed well over the last few years and looks set to continue, mainly due to the ongoing demand for grade A office space and the limited supply available.

Q: How did the leasing market finish in 2024?

A: 2024 ended on a strong note, with leasing activity 17% ahead of the long-term average of 2.8 million sq. ft. It's been an excellent year overall for the leasing market.

Q: What type of space is in the highest demand in the leasing market?

A: About 71.3% of leasing take-up has been for new and refurbished spaces. There’s a lot of activity in the 40,000 to 60,000 sq. ft floorspace range, particularly driven by the Professional and Financial Services sectors. If the Technology sector also picks up, we could see even more demand from a broader range of sectors.

Q: Could you share some notable deals that have happened in the financial and professional services sectors?

A: Well, in Q4, we saw two major deals in the City, at 10 Gresham Street and One Millennium Bridge, both involving outstanding refurbishments or partial reconstructions. These spaces attracted world-class occupiers, with both deals achieving very strong rents.

Active Demand and Vacancy Rates

Q: How is demand for office space in London right now?

A: Demand is over 18% above the long-term average, which is a positive indicator for the market.

Q: What are the current vacancy rates, and how do they impact the market?

A: Vacancy rates are extremely low. In the City Core, the vacancy rate for new office space is less than 1%, and the same goes for the West End Core. When you factor in new and refurbished space, both areas have vacancy rates under 4%. This scarcity of Grade A space is pushing rents up, which is a clear sign of a tight market.

Q: How does the low vacancy rate affect rents?

A: The low vacancy rate, especially when you consider that 71% of take-up is in the new and refurbished sector, is a significant factor driving rents up. This concentration of demand in a small pool of available space is creating upward pressure on prices.

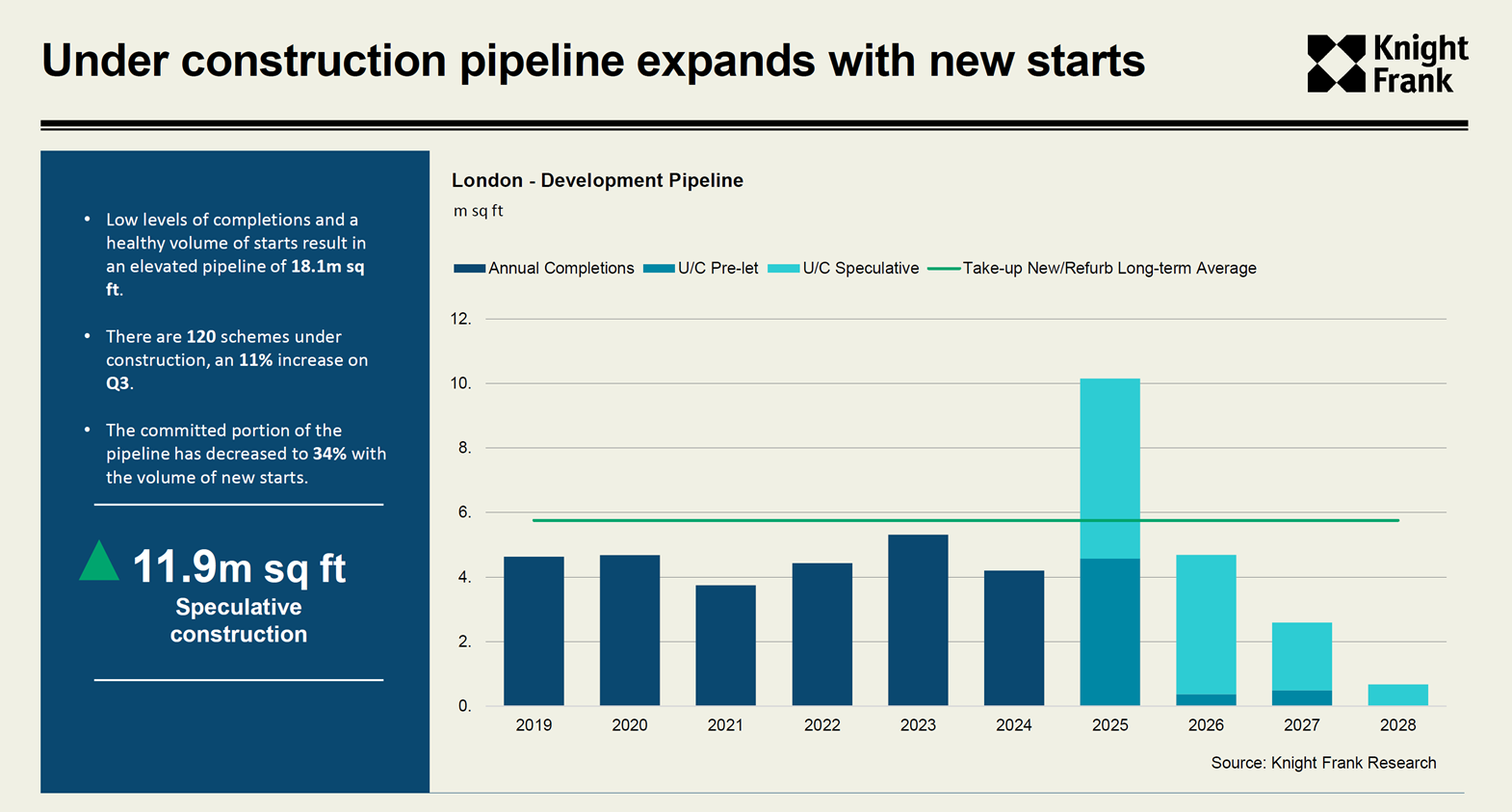

Q: Is this low vacancy rate affecting construction in the market?

A: Yes, it is. The low vacancy rate is fuelling a strong construction pipeline, but as you can see from our data, there’s not enough speculative office space being delivered over the next four years to meet demand.

Q: How have submarkets responded to these trends?

A: The City Core has performed very well, especially in Q4. There’s still development underway, and we've seen prime rents increase from £90 to £95 per sq. ft. The market here is responding strongly to the demand for new and refurbished office spaces.

Q: Finally, what’s your overall outlook for the London office market moving forward?

A: The outlook remains positive, with strong demand continuing across sectors. While there are challenges in terms of supply, the market dynamics suggest we’re in for more growth, particularly in high-demand areas like the City and West End. The combination of limited Grade A space and ongoing demand is a key driver for the next few years.

To find out more about how we work with clients to attain their goals, contact the London Office Leasing team. To contact Dan Gaunt directly, get in touch.

Knight Frank Newcastle

Knight Frank Newcastle is recognised as one of the most progressive and dynamic commercial property estate agent in the region and North East.